09/06/22, Lehman Brothers bankruptcy

Our first bankruptcy!

Hello all, and welcome to day three of this journey! You might be getting tired of that introductory message - tough shit.

I’m still collecting feedback from you guys, and conciseness seems to be the name of the game. In that nature, I’m aiming for an even shorter reading time than previously, so you can devour this in a 2 minute frenzy.

In other news, I may shift to 3-newsletters-a-week model. This isn’t because I don’t have the time, those of you who know me can attest to my neurotic work schedule. Rather, spreading out these newsletters ensures I can include interviews that I have lined up (spanning PE, law, IB so far!). These interviewees understandably need to clear the content before I send it out, and doing so within 24 hours is nigh on impossible. I’ll decide by Friday. With that being said, let’s dive in!

Outline

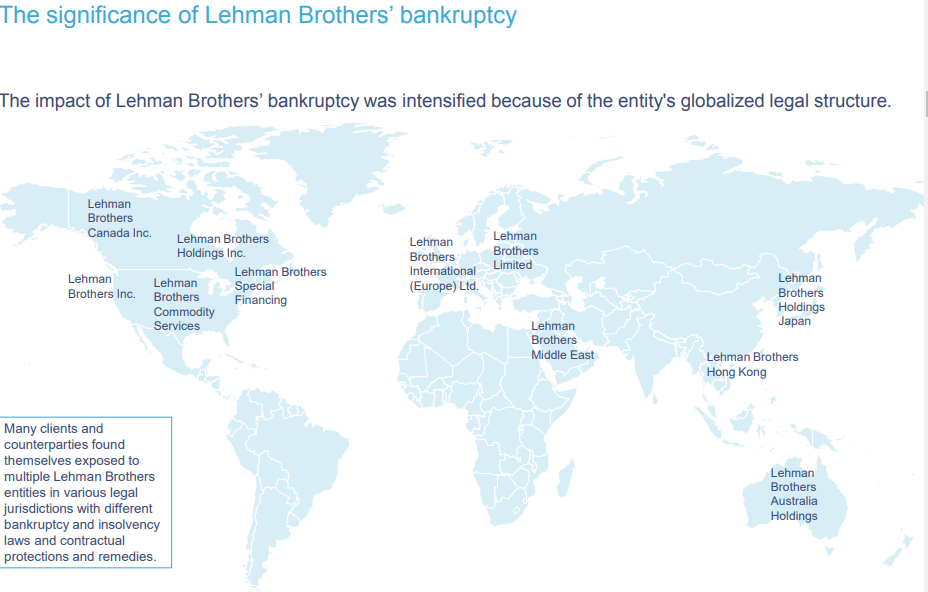

Today, I bring you a chronicle as old as… well… 2008: the Lehman Brothers collapse. But first, critically analyse this image and try to infer what possibly went wrong:

Lehman was a world-leader in trading complicated financial products that were betting, amongst other things, that house prices would continue to rise (mortgage-backed securities). What could possibly go wrong? Well, in 2008, house prices slumped, and the immense amount of leverage Lehman had assumed through these products led to them going bankrupt. Cue a cataclysmic obliteration of Lehman’s balance sheet - a depreciation so rapid it makes your crypto portfolio returns look pleasant.

As a Greek, I am all too familiar with debt, but let’s go through the timeline and I’ll show you how the bankruptcy process with Lehman put my motherland to shame.

Timeline

1997 - 2003: Lehman ventures into mortgage origination (providing mortgages), buying incumbents Alt-A and BNC Mortgage in 1997 and 2000 respectively. Importantly, Lehman specialises in sub-prime mortgages (borrowers with low credit ratings).

2004: Lehman does $3b/month of subprime lending.

2006: Lehman does $50b/month of subprime lending.

2008: Lehman has assets of $680b, but firm capital of only $23b. With this debt-to-equity ratio, a 3% decline in house prices would wipe out Lehman’s portfolio (how did no one see this??)

June 2008: Lehman shows losses of $3b in second fiscal quarter results, stemming from sub-prime exposure, share price drops 73% over same this half of the year.

September 2008: Faeces hits the fan. Shares drop 45% in one day as it becomes clear Lehman’s potential saviour, the Korea Development Bank, was not able to provide assistance. Things start moving very quickly here. On September 12th, the Fed meets with all the major Wall Street banks to discuss a rescue deal. Nothing comes to fruition. On September 14th, Barclays’ bid to save Lehman falls through, and Lehman, represented by Weil, file for Chapter 11 bankruptcy.

Breakup process: in the following months, parts of Lehman get sold to Barclays and Nomura. Most of the carcass gets liquidated to appease creditors.

I end this timeline with a quotation from Judge Peck, the man in charge of the bankruptcy hearings, talking about his decision to approve Barclays’ purchase of Lehman’s office:

‘I have to approve this transaction because it is the only available transaction. Lehman Brothers became a victim, in effect the only true icon to fall in a tsunami that has befallen the credit markets. This is the most momentous bankruptcy hearing I've ever sat through. It can never be deemed precedent for future cases. It's hard for me to imagine a similar emergency.’

Analysis

I’m now going to touch on why this bankruptcy proceeding was so poorly managed. Filing for bankruptcy is an acceptable strategy as long as it delivers financial value in the long-run. This sounds moronic, but it’s not. Bankruptcy protection, at least in the US, stops creditors trying to seize assets in the short-run and gives the firm time to restructure debt to extend payment deadlines, for example.

Unfortunately, Lehman Brothers destroyed even more shareholder value during the bankruptcy proceedings for multiple reasons:

Chaotic filing: Lehman Brothers is actually hundreds of different entities across the world. One would hope a bank of this size would have procedures in place to co-ordinate massive financial restructuring. This was not the case. 75 different bankruptcy proceedings occurred - pure madness.

Bankruptcy rules for financial institutions: in the US, bankruptcy law means derivative portfolios can either be sold as a whole, or as one-by-one contracts. Lehman could not sell chunks of its portfolio to different parties. Seeing as this portfolio was in the 100’s of billions, no one could purchase it as a whole. Thus, Lehman essentially conducted a fire sale to sell of their individual contracts at any price possible - not nice, methinks.

Uniqueness of situation: Bankruptcies often work because they are predictable. However, Lehman’s size, exposure to derivatives, and position as a bank meant it was a precedent-setting bankruptcy. I’ll give one example, but more can be found in the New York Fed further reading. The absolute priority rule means creditors (bondholders, etc) always rank ahead of equity holders (stockholders, etc). In some cases, this rule is inverted so equity holders rank first. However, Lehman was the first instance in which the absolute priority rule distinguished between different classes of creditors, with creditors of derivate sections of Lehman being ranked below creditors of Lehman as a general corporation. Stuff like this complicated the proceedings massively and highlights that no financial mechanism is ever wholly predictable, regardless of existing legal provisions.

Thank you for reading!

Well, that wraps up day 3 of the operation. Good job getting this far, the legal bits of this deal are pretty complex. I find it exciting, but I also do quizzes for fun so no surprises there. Also, I want everyone to try and give a gift subscription after reading this. The more readers the better, and I want to have as many as possible before I bring in some really, really, cool guests.

Love you all,

Alex

Further readings

Investopedia, ‘The Collapse of Lehman Brothers: A Case Study’

PWC, ‘Lehman Brothers’ Bankruptcy: Lessons learned for the survivors’