26/08/22, Herbalife

Two investors bully eachother on TV, Herbalife gets caught in cross-fire.

Hello everyone, long time no see. I would like to explain my hiatus by saying I was conducting some deep research on emerging markets and hedge fund strategies.

However, that would be lying.

I have spent the past month and a bit gallivanting around the Mediterranean, Baltics and South West London. Everyone needs rest. Now I’m back.

I missed you all greatly, and am fully recharged and ready to pump out analysis in preparation for your applications, professional development, or general curiosity. Everything that came before this was me figuring out how to do the newsletter - a test-run of sorts. Now I’m here for good.

With that being said, let’s dive in!

Deal Outline

Summary: one hedge fund manager (Bill Ackman) shorts Herbalife, arguing Herbalife is a pyamid scheme, and should be shut down. Another hedge fund manager (Carl Icahn, who has prior beef with Ackman) goes long on Herbalife, saying it has good fundamentals and is not a pyramid scheme. What ensues is a very public spat, years of litigation, and Ackman ultimately losing out - financially and reputationally.

Relevant parties:

Bill Ackman and Pershing Square Capital Management: Pershing Square runs activist campaigns against big companies, like McDonald’s and Wendy’s. With around $20b AUM, Pershing Square is one of the more reputed activist funds. Bill Ackman is revered for his investing skills and youthful appearance in equal measure.

Carl Icahn and Icahn Enterprises: Icahn owns a large majority of Icahn Enterprises - a conglomerate, not a fund. Thus, Icahn does not have the same fiduciary duties and obligations to investors that Ackman does, meaning he often comes across as brash and more self-interested than traditional financiers. Like Ackman, Icahn is known to wage his own activist campaigns. Currently, Icahn Enterprises has around $25b of assets.

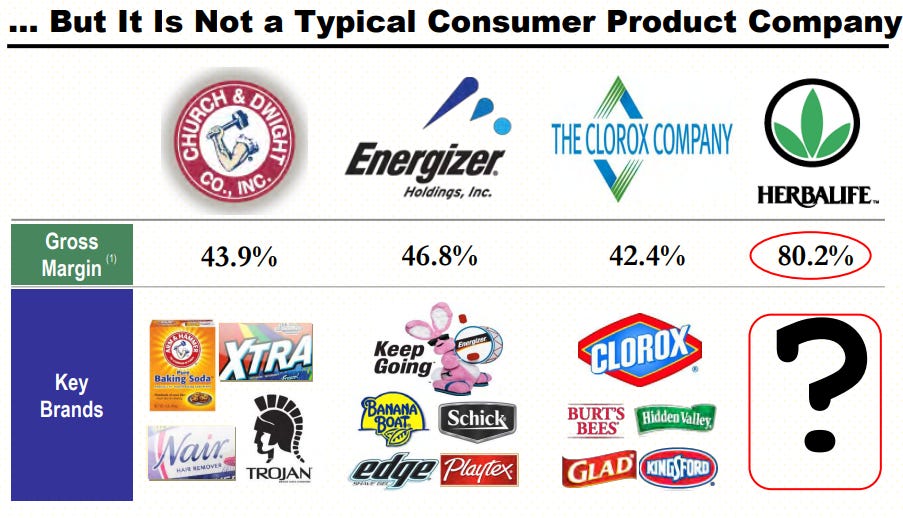

Herbalife: Herbalife is around today, and doing pretty well. 2021’s annual report indicated around $6b in revenue and around $500m in net income. Essentially, Herbalife sell simple consumer goods, like vitamins. However, they do so by selling bulk amounts of goods to ‘distributors’, (i.e. random people) who are then entrusted to sell the goods on for a profit. This model is called multi-level marketing; it is not always illegal, but it is certainly unsavoury. It is this business structure that makes Herbalife such a unique company.

To sum up Ackman’s issue with Herbalife, I refer to Pershing Square’s investor presentation:

‘Herbalife is in the business of selling dreams, not weight-management products.’

Strap in, this is about to get messy.

Deal Analysis

Ackman’s thesis

Ackman’s argument was simple.

Herbalife is a pyramid scheme;

Pyramid schemes are illegal;

Illegal business structures inevitably fail.

They die either at the hands of the law (forced break-up) or at their own hands (pyramid schemes are always bound to fail, as there will eventually come a time where there are no more ‘distributors’ left to recruit).

As seen above, the inclusion of distributors in the business model improved margins significantly; Herbalife was effectively getting free labor that made it appear far more successful than its competitors.

The dispute

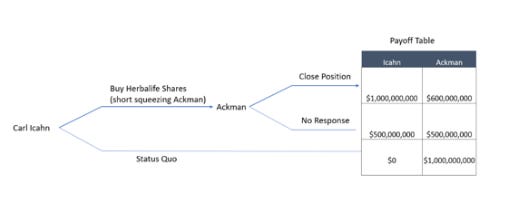

In December 2012, Ackman announces the short, rumoured to be around $1b. Next month, Icahn’s stake is revealed. Remember: a short-seller earns money if the price of a stock goes down, whereas Icahn earns money if the price goes up. Ackman previously triumphed in a legal dispute over Icahn, adding a personal/reputational element to this Herbalife investment.

The ensuing mixture of volatile emotions and high stakes led to a showdown between the two on CNBC. I highly recommend you watch it - at some points, you can hear the traders from the trading floor below the CNBC studios roaring with interest as Ackman and Icahn trade insults. This event was similar to the two popular kids fighting during lunch-time at school, but replace the kids with billionaire men in Hugo Boss suits and replace the punches with snide remarks and costly court cases.

Icahn says at one point:

‘He probably woke up one morning and said let’s see which company we can destroy.’

Icahn basically argues Ackman has no reason to short Herbalife, other than to create fear amongst other investors who respect Ackman, which will reduce the price of Herbalife stock in itself (thus making Ackman money).

Ackman had shorted Herbalife stock in the mid-forty-dollar range. After his 300-slide presentation critiquing Herbalife, the stock had slid to the mid-twenties. Ackman could have closed the trade there and netted hundreds of millions.

This wouldn’t be a very interesting story if that had happened.

Instead, Ackman clung on as the value dropped until…

…other investors started buying Herbalife stock, believing it was undervalued. Dan Loeb of Third Point and, eventually, Carl Icahn, begin boosting the Herbalife stock price, effectively ‘short squeezing’ Ackman. The more the Herbalife stock price rose, the more Ackman lost.

By March 2018, Ackman had fully exited the trade, losing his investors hundreds of millions.

Why did Ackman fail?

This is a tale of two parts: optics and reality.

Optics: Ackman comes across as the force for good. Ackman portrays himself as exposing a fraudulent company that he believes is exploiting vulnerable distributors. He even pledges to donate his profits from the investment to charity. Seems quite noble for an industry famed for ruthlessness. The CNBC dispute with Icahn is widely viewed as an Ackman victory - Icahn stutters, tells the host to ‘stop interrupting’; Ackman calmly deploys facts and wit.

Reality: Over 5 years, Icahn’s stake nets him hundreds of millions and Ackman loses hundreds of millions.

Being right does not always mean you win. After considerable lobbying by Ackman, the FTC investigated Herbalife, who ended up settling for around $200m and having to make some pretty substantial changes to their business. Ackman was partially right in alleging Herbalife was operating against the law.

But name me one company of Herbalife’s size that has a clean legal sheet. Just because Herbalife had some legal liabilities, that didn’t mean it was worth nothing.

Ultimately, I would argue Ackman got too emotionally invested in his Herbalife short - he cries during the investor presentation, pledges money to charity, and is going up against a guy he doesn’t really like (Icahn).

In doing so, Ackman placed the nails in his own coffin (is that too dramatic?).

Fast forward a few years, Ackman and Icahn hug it out at a conference. I guess consistently excellent risk-adjusted returns really do wash away any feelings of animosity after a few years.

Key takeaway: every generic finance youtuber says ‘don’t invest based on emotion’. Now you can see why that advice is actually pretty useful.

Thank you for reading!

Listen, I’ve been gone for a while - sorry for that. I love writing these and I hope you enjoyed today’s edition. Any questions whatsoever, do reach out!

Side note - watch ‘Industry’ on HBO/Sky. Entertaining but accurate portrayal of life as a young investment banker.

Love you all.

Further readings

Herbalife, Annual Investor Report 2021

Madison Business Review, ‘Short squeeze: The game theory of a billion-dollar bet’

Pershing Square, ‘Who wants to be a millionaire?’ (investor presentation announcing the short - not for the faint-hearted)

The New Yorker, ‘Financiers Fight Over the American Dream’ (incredible journalism)